![]()

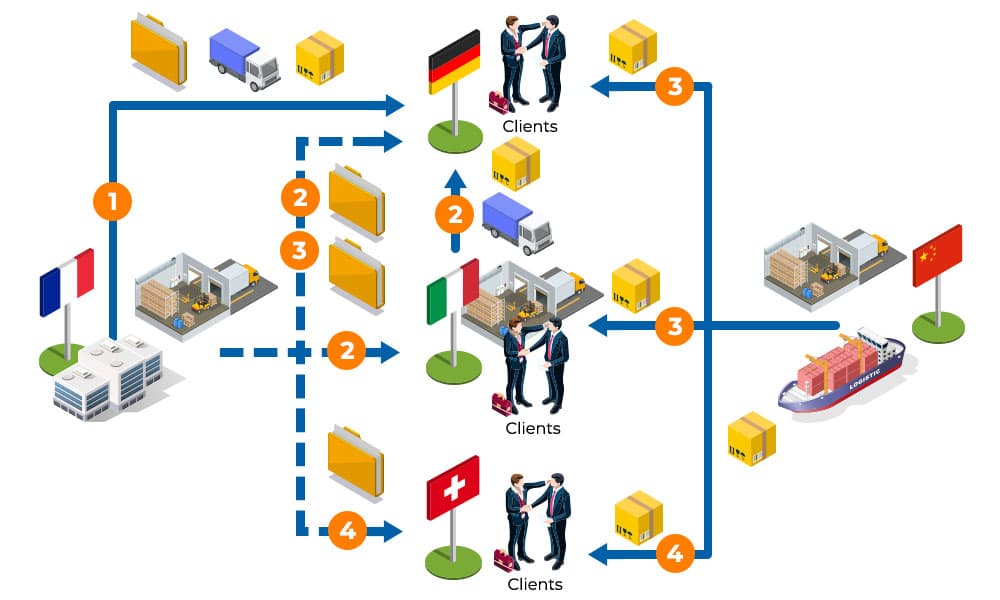

Simple Intra-Community Distance Selling (IDS)

You deliver to private individuals in Spain from your warehouse in France, where you are based. 2 scenarios:

- Your turnover excluding VAT from Intra-Community distance selling during the year N-1 or N is less than the EUR 10,000 threshold: you invoice including VAT (French VAT).

- Your turnover excluding VAT from Intra-Community distance selling during the year N-1 or N is higher than the EUR 10,000 threshold: you invoice including VAT (Spain VAT).

To declare and pay back the Spain VAT collected you have two options:

- Register with the One-Stop-Shop in your country of residence (France), declare and pay VAT via the EU OSS portal.

- Register for VAT in Spain and file a Spain VAT return.

Please note: you are liable for INTRASTAT on dispatch in France if your dispatch sale threshold of EUR 460,000 is exceeded. If the threshold for introduction into Spain IS exceeded, you may be liable for INTRASTAT on introduction into Spain.

![]()

Intra-Community distance selling with remote stock

You deliver to private individuals in Spain from your warehouse in Italy. 2 scenarios:

- Your turnover excluding VAT from Intra-Community distance selling during the year N-1 or N is less than the EUR 10,000 threshold: you invoice including VAT (Italian VAT).

- Your turnover excluding VAT from Intra-Community distance selling during the year N-1 or N is higher than the EUR 10,000 threshold: you invoice including VAT (Spanish VAT).

To declare and pay back the collected VAT when the threshold is exceeded, you have two options:

- Register with the One-Stop Shop from your country of residence (France) and declare your Intra-Community distance sales from the EU OSS portal. Please note: you must be registered in the country where you hold your stock (Italy) if you make domestic purchases/sales, Intra-Community acquisitions, imports or stock transfers from your stock.

- Obtain a VAT numberin Italy and Spain and file your returns locally.

Please note if you exceed the INTRASTAT threshold for shipment to Italy, you will need to file an INTRASTAT return in Italy. The same is true in Spain with the INTRASTAT threshold at introduction.

![]()

Distance selling by dropshipping to customers in EU countries

You buy in China and deliver directly to your customers in Spain or Italy without going through a storage platform: this is called dropshipping.

For direct deliveries from China to your private customers in Spain and Italy, two scenarios are possible:

- Imported goods with a consignment value lower than EUR 150 per parcel: you can register with the one-stop-shop and declare these transactions through your IOSS portal. If your transactions are carried out through a marketplace , these transactions must be declared through the marketplace‘s one-stop shop (IOSS portal).

- Imported goods with a consignment value higher than 150 euros per package: you must identify yourself for VAT in the countries where the goods are imported (Spain and Italy) and complete the customs and VAT formalities.

![]()

Distance selling by dropshipping to customers located in a country outside the European Union

For direct deliveries from China to your private individuals in Switzerland, you will probably have to take care of the customs formalities on import. To pay local taxes and duties you will have to register for VAT in Switzerland.