![]()

Intra-Community acquisition subject to VAT in Italy.

You must provide your German supplier with your Italian VAT number. The purchase is considered an Intra-Community acquisition subject to Italian VAT – to be declared on your Italian VAT returns.

![]()

Domestic sales subject to VAT in Italy.

In the case of Italy, you will invoice your customer without VAT, as Italy has opted for the reverse charge system.

Your tax-free sale may not have to be declared on your Italian VAT returns.

Note: this system varies from country to country.

General rules and special cases:

There are two scenarios depending on the legislation in force in the country where the domestic sale is made:

- The general rule: you will have to invoice your customer including VAT (at the VAT rate in force in their country) and will file your VAT return in that country for all your operations (purchases and sales).

- The reverse charge mechanism)

Some Member States will apply the reverse charge mechanism to domestic deliveries made on their territory. In this scenario, it is the purchaser who will be liable for the VAT, not the seller. Depending on the country, this purchaser must have a VAT number and/or be established in the country where the delivery is made.

Please note: even if the country where you deliver has opted for the reverse charge mechanism, you will still have to register for VAT for Intra-Community acquisitions (transaction 1 above)!

Domestic purchase of goods in Spain from a supplier in Spain :

If you buy the goods in Spain, you will be charged including Spanish VAT at the current VAT rate in Spain for the item concerned. This input VAT can be deducted on the VAT returns that you have to file in Spain.

![]()

Sale of goods to a customer in Italy:

If your customer is registered for VAT in Italy, you are making an Intra-Community supply that is exempt from Spanish VAT.

You will need to file a Spanish VAT return, a Spain EC SALES LIST return and a Spain INTRASTAT return on dispatch if the threshold is exceeded. In addition, you will have to comply with the Spanish obligations in terms of invoicing and proof of exemption.

![]()

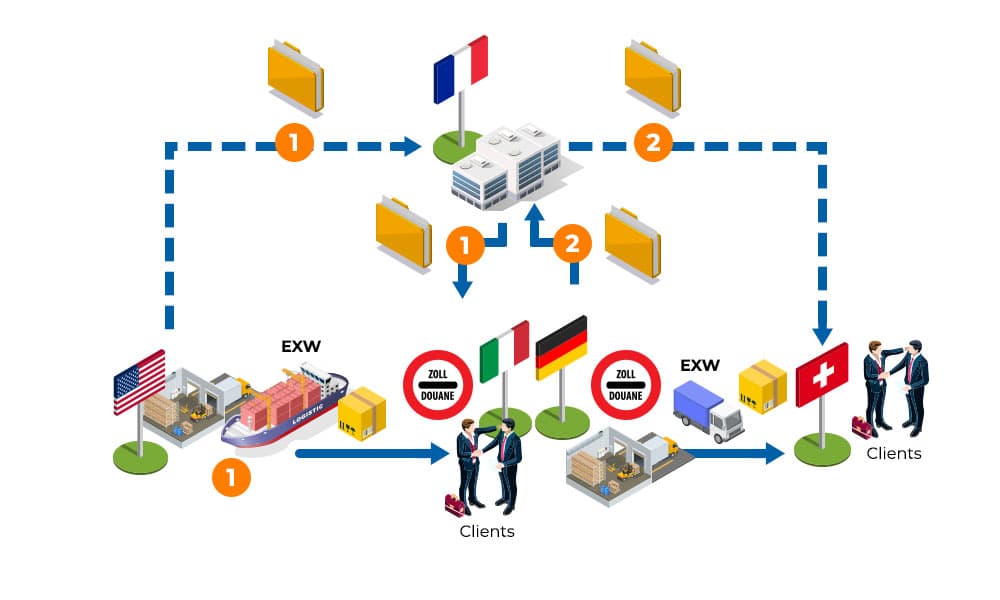

Triangular import (USA > Italy)

When you are an importer in a Member State of the European Union (Italy), you must register for VAT in the arrival Member State (Italy).

![]()

Triangular export (Spain > Switzerland)

If you are acting as an exporter of records from an EU Member State, (Spain), you must register for VAT purposes in the departure Member State (Spain).