A summary by the experts

Both passenger transport services and renting modes of transport are subject to VAT within the European Union, but follow different rules:

1> Passenger transport services within the European Union are subject to VAT in each country according to the distances covered. This rule applies to road transport. Air and sea transport from and to foreign countries is in most cases exempt from VAT. As the regulations for these types of transport are rather complex, we suggest you contact an expert.

2> When a mode of transport is rented for a short period of time VAT is due at the place where the transport is provided. The place of provision is understood to be the place where the hirer takes possession of the transport or the place where a third party takes possession of the transport on behalf of the hirer. “Short term” means less than 30 days for a road or air transport, less than 90 days for sea transport.

![]() The service must be correctly qualified to determine the applicable rules. This qualification can be complex in some cases, such as for car rental with a driver or yacht rental with a crew.

The service must be correctly qualified to determine the applicable rules. This qualification can be complex in some cases, such as for car rental with a driver or yacht rental with a crew.

![]()

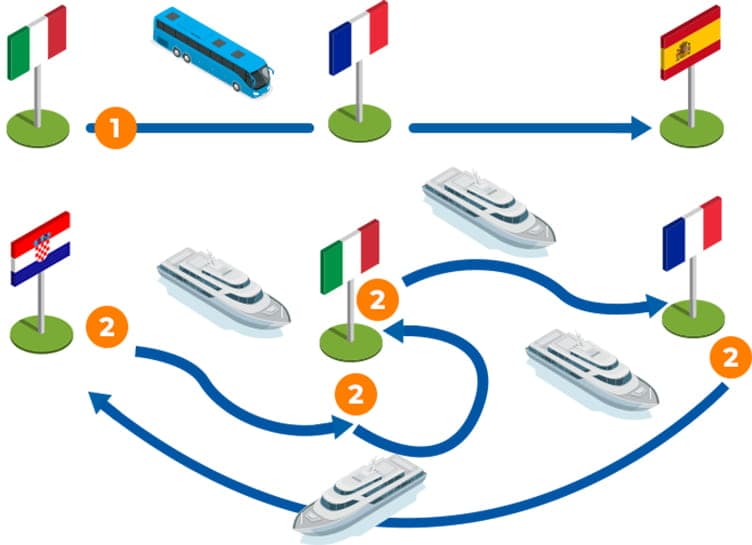

Transporting people

The price of the ticket must be divided in proportion to the distances travelled in each of the countries, and subject to Spanish, Italian and French VAT.

![]()

Renting a means of transport

You are a company that owns yachts and you carry out week-long charters with availability in Croatia, Italy and France.

This activity is subject to the VAT rules relating to the rental of short-term means of transport.